Training can modify strategy parameters, generate trading rules, and assign optimal capital allocation factors for profit reinvestment or portfolio distribution. Here's a short introduction to algo system training.

For preparing a parameter based strategy to be trained, set the PARAMETERS flag and assign optimize calls to all optimizable parameters. The code for training the SMA time period of a simple moving average crossover system would look like this:

// n-bar Moving Average system (just for example - don't trade this!)

function run()

{

set(PARAMETERS);

var TimePeriod = optimize(100,20,200,10);

vars Prices = series(price());

vars Averages = series(SMA(Prices,TimePeriod));

if(crossOver(Prices,Averages))

enterLong();

else if(crossUnder(Prices,Averages))

exitLong();

}

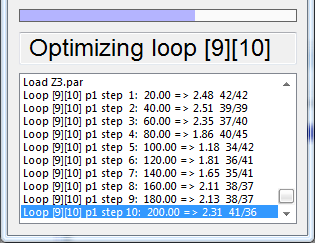

Now click [Train]. Zorro will now run through several optimization cycles for finding the most robust parameter combination. Zorro optimizes very fast; still, dependent on the number of parameters, assets, and trade algorithms, optimization can take from a few seconds up to several hours for a complex portfolio strategy. The progress bar indicates the time you have to wait until it's finished:

The displayed values per line are the loop and parameter number, the optimization step, the parameter value, the result of the objective function, and the number of winning and losing trades.

In [Train] mode, trades usually open 1 lot, regardless of Lots or Margin settings. The results are summed up over all sample cycles. Pool trades are not used, and phantom trades are treated like normal trades. This behavior can be modified for special cases with TrainMode flags.

The optimal parameters are stored in a *.par file in the Data folder, and are automatically used by Zorro when testing or trading the system. Parameters are normally optimized and stored separately per asset/algorithm component in a portfolio system; therefore all optimize calls must be located inside the asset/algo loop if there is any. When the FACTORS flag is set, capital allocation factors are also generated and stored in a *.fac file in the Data folder. When the strategy contains advise calls and the RULES flag is set, decision tree, pattern detection, or perceptron rules are generated and and stored in *.c files in the Data folder. If external machine learning functions are used, the trained models are stored in *.ml files in the Data Folder. In [Train] mode, trades usually open 1 lot, and pool and phantom trades are converted to normal trades (unless special TrainMode flags are set). Parameters, factors, and rules can be generated either together or independent of each other.

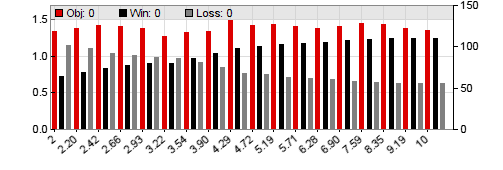

Training shows if the strategy is robust, i.e. insensitive to small parameter changes. Therefore it goes hand in hand with strategy development. When training a strategy in Ascent mode with the LOGFILE flag set, Zorro shows the performance variance over all parameter ranges in parameter charts on a HTML page, like this:

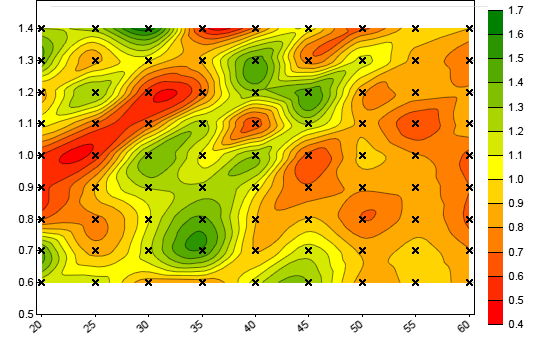

The charts are stored in the Log folder and end with the number of the parameter, f.i. _p1 for the first, _p2 for the second parameter and so on. The red bars are the result of the objective function, which is by default the profit factor of the training period, corrected by a factor for preferring a higher number of trades. The grey bars show the number of losing trades and the black bars show the number of winning trades. In walk forward optimization, the parameter charts display the average results over all WFO cycles. Genetic or brute force optimization does not generate parameter charts, but contour plots from the first two parameters as shown below.

Training is critical for almost all strategies, and should not be omitted even when a strategy appears to be already profitable with its default parameters. Most strategies only work within certain parameter ranges. Those ranges are usually different for every asset and also vary with the market situation - a bullish or bearish market requires different parameters than a market in a sidewards phase. Due to the asymmetry of many markets, long and short trades often also require different parameters. Naturally, parameters can only be optimized to a specific historical price curve, therefore they perform best with that particular price curve and will perform not as good with any other data - such as real time prices in live trading. This effect is called overfitting. It varies with the strategy, and is discussed below.

Select carefully the parameters that you train. Parameters that depend on external events - for instance, the market opening hour when the strategy exploits the overnight gap - must never be trained, even if training improves the test result. Likewise, parameters that should have no effect on strategy performance, such as price patterns from long ago or the start date of a backtest, must never be trained. Otherwise you're in danger to replace a real market inefficiency by a random training effect.

For avoiding overfitting bias when testing a strategy, parameter values are typically optimized on a training data set (the "in-sample" data), and then tested on a different data set (the "out-of-sample" or "unseen" data) to simulate the process of trading the system. If the optimized parameters do not perform well on out-of-sample data, the strategy is not suited for trading. Zorro offers several methods for optimizing and testing a strategy with unseen data:

This method divides the price data into one-week segments (a different segment length can be set up through DataSkip). Usually two of every three weeks are then used for the optimization, and every third week is skipped by the optimization and used for the strategy test. The LookBack period is the part of the price curve required for functions that use past price data as input, such as moving averages or frequency filters. Thus a preceding lookback period is always cut off in front of the data for both training and testing.

|

Simulation period

|

||||||||||

LookBack |

Training |

|||||||||

Test |

||||||||||

For setting up this method, set different SKIP1, SKIP2, SKIP3 flags for training and testing. Usually, SKIP3 is set in train mode and and SKIP1+SKIP2 in test mode; any other combination will do as well as long as two weeks are used for training and one week for testing. A script setup for horizontal split optimization looks like this:

function run() // horizontal split optimization

{

if(Train) set(PARAMETERS+SKIP3);

if(Test) set(PARAMETERS+SKIP1+SKIP2);

...

}

Horizontal split optimization is good for quick tests while developing the strategy, or for testing when you don't have enough price data or enough trades for walk-forward optimization. It is the fastest method, uses the largest possible data set for optimization and test, and gives usually quite realistic test results. For checking the consistency you can test and train also with different split combinations, f.i. SKIP1 for training and SKIP2+SKIP3 for testing. The disadvantage is that the test, although it uses different price data, runs through the same market situation as the training, which can make the result too optimistic.

Alternatively, you can select only a part of the data period - such as 75% - for training. The rest of the data is then used exclusively for testing. This separates the test completely from the training period. Again, a lookback period is split off for functions that need past price data.

|

Simulation period

|

|||||

LookBack |

Training

|

Test |

|||

For setting up this method, use DataSplit to set up the length of the training period. A script setup for vertical split optimization looks like this:

function run() // vertical split optimization

{

set(PARAMETERS);

DataSplit = 75; // 75% training, 25% test period

...

}

Vertical split optimization has the advantage that the test happens after the training period, just as in live trading. The disadvantage is that this restricts testing to a small time window, which makes the test quite inaccurate and subject to fluctuations. It also does not use the full simulation period for optimization, which reduces the quality of the parameters and rules.

For combining the advantages of the two previous methods, an analysis and optimization algorithm named Walk Forward Optimization (WFO in short) can be used. This method is a variant of cross-validation and was first suggested for trading strategies by Robert Pardo. It trains and tests the strategy in several cycles using a data frame that "walks" over the simulation period:

WFOCycle |

Simulation period |

||||||||

1 |

LookBack |

Training |

Test1 |

||||||

2 |

LookBack |

Training |

Test2 |

||||||

3 |

LookBack |

Training |

Test3 |

||||||

4 |

LookBack |

Training |

Test4 |

||||||

5 |

LookBack |

Training |

|||||||

| OOS Test | LookBack |

Test5 |

|||||||

| WFO Test | Look |

Back |

Test1 |

Test2 |

Test3 |

Test4 |

|||

WFOCycle |

Simulation period |

||||||||

1 |

LookBack |

Training |

Test1 |

||||||

2 |

LookBack |

Training |

Test2 |

||||||

3 |

LookBack |

Training |

Test3 |

||||||

4 |

LookBack |

Training |

Test4 |

||||||

5 |

LookBack |

Training |

|||||||

| Test | Test1 |

Test2 |

Test3 |

Test4 |

|||||

The parameters and rules are stored separately for every cycle in files ending with "_n.par" or "_n.c", where n is the number of the cycle. This way the strategy can be tested repeatedly without having to generate all the values again. The test cycle is divided into (n-1) test periods that use the parameters and factors generated in the preceding cycle. The last training cycle has no test period, but can be used to generate parameters and rules for real trading.

For setting up this method, use DataSplit to set up the length of the training period in percent, and set either NumWFOCycles to the number of cycles, or WFOPeriod to the length of one cycle. A script setup for Walk Forward Optimization looks like this:

function run() // walk forward optimization

{

set(PARAMETERS);

DataSplit = 90; // 90% training, 10% test

NumWFOCycles = 10; // 10 cylces, 9 test periods

...

}

The WFO test splits the test period into several segments according to the WFO cycles, and tests every segment separately. The test result in the performance report is the sum of all segments. The parameters from the last cycle are not included in the WFO test as they are only used for real trading. A special OOS test can be used for out-of-sample testing those parameters with price data from before the training period.

WFO can be used to generate a 'parameter-free' strategy - a strategy that does not rely on an externally optimized parameter set, but optimizes itself in regular intervals while trading. This makes optimization a part of the strategy. WFO simulates this method and thus tests not only the strategy, but also the quality of the optimization process. Overfitted strategies - see below - will show bad WFO performance, profitable and robust strategies will show good WFO performance. The disadvantage of WFO is that it's slow because it normally runs over many cycles. Like vertical split optimization, it uses only a part of the data for optimizing parameters and factors. Depending on the strategy, this causes sometimes worse, sometimes better results than using the full data range. Still, WFO is the best method for generating robust and market independent strategies.

Another advantage of WFO is that training is a lot faster than the other methods when using several CPU cores.

If a machine learning strategy also requires training of parameters, several training cycles in a certain order are required. There are several possible scenarios:

NumTrainCycles = 2; if(TrainCycle == 0) set(RULES,PARAMETERS); // Test or Trade mode else if(TrainCycle == 2) set(PARAMETERS); else if(TrainCycle == 1) set(RULES);

if(Train) set(RULES,PARAMETERS); else set(RULES);

set(RULES,PARAMETERS);

Training rules and parameters at the same time only works with single assets, not with a portfolio system that contains loops with asset or algo calls. If required, train all portfolio components separately and combine the resulting .c files. The Combine.c script can be used as a template for automatically combining parameters and rules from different assets or algos. Machine learning models (.ml files) can be combined with an appropriate R function. With Zorro S, the process can be automatized with a batch file.

When training a portfolio of assets and algorithms, it is normally desired to train any asset/algo component separately, since their parameters and rules can be very different. Only in special cases it could make sense to train parameters that are common to all components, or use a combination of commonly and separately trained parameters. Examples for all 3 cases can be found under loop.

Before training a system the first time, make sure to run a [Test] with the raw, unoptimized script. Examine the log and check it for error messages, such as skipped trades or wrong parameters. You can this way identify and fix script problems before training the script. Training won't produce error messages - trades are just not executed when trade parameters are wrong.

Money management or profit reinvesting should not be active for training strategy parameters, because it would introduce artifacts from the different weights of trades. For this reason training uses fixed-size trades by default. If you want to train a money management algorithm or use different lot sizes, do that in a separate step using the TRADES flag after all other parameters have been trained.

After training, files are generated which contain the training results and the generated rules, parameters, and factors (see Export). A Zorro strategy can thus consist of up to 4 files that determine its trading behavior:

All 4 files, except for the executable *.x and the *.ml machine learning models, are normal text files and can be edited with any plain text editor.

The optimizing process naturally selects parameters that fare best with the used price data. Therefore, an optimized strategy is always more or less 'curve fitted' to the used price curve, even with Zorro's range-based optimizing. Neural networks, genetic algorithms, or brute force optimization methods tend to greatly overfit strategies. They produce panda bears that are perfectly adapted to a specific data set, but won't survive anywhere else. Some suggestions to reduce overfitting:

► latest version online